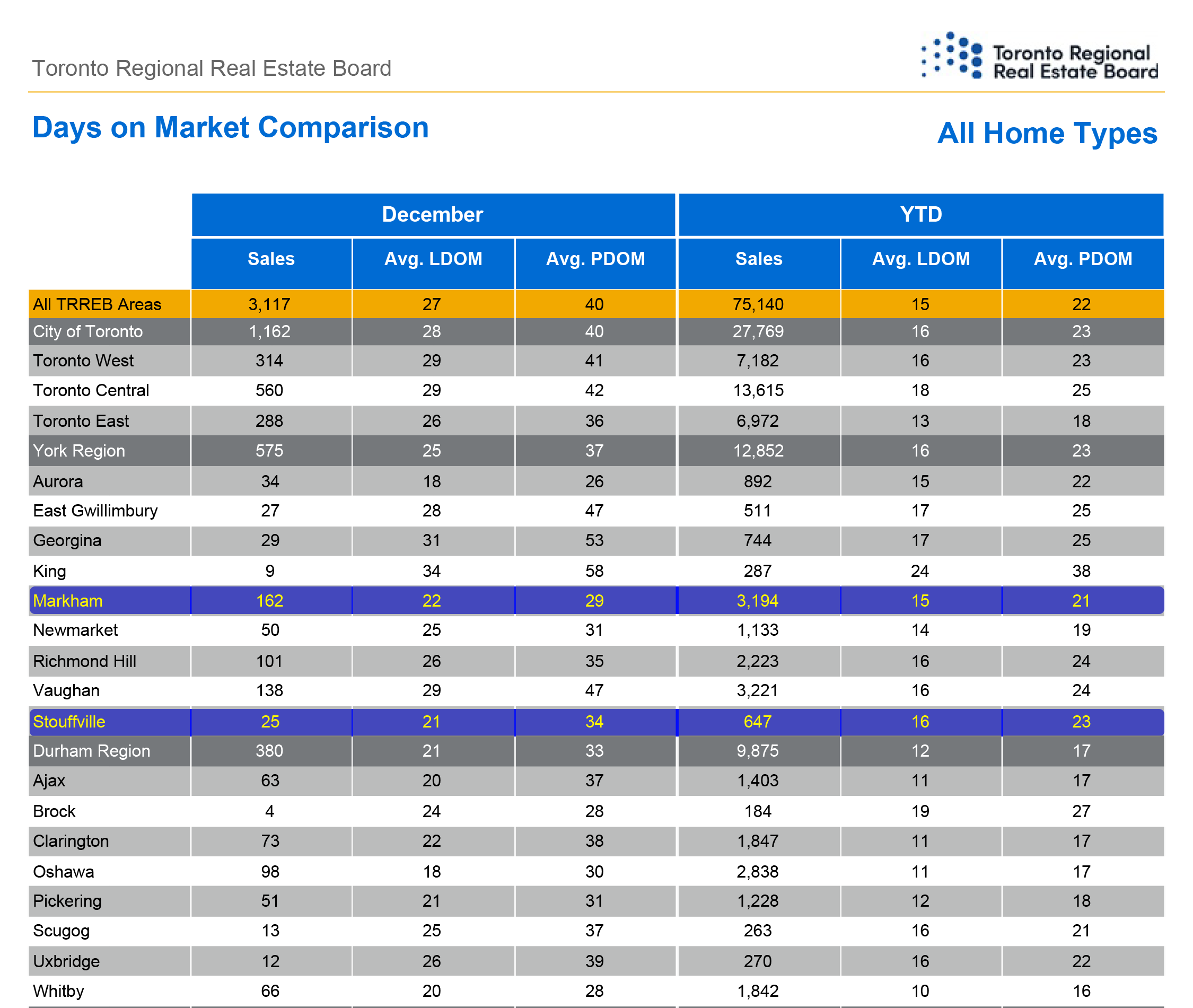

t hasn't been in the mainstream news much yet, but Phase 2 of the updated "TRESA" Trust in Real Estate Services Act - which dictates guidelines for Real Estate transactions in Ontario, is being implemented as of December 1st.

TRESA Phase 2

These changes have significant impact on how you will (or will not) be working with your chosen Realtor, and offers some additional choices for both Buyers and Sellers in their transactions.

Currently, as a Realtor, we have options to work with Buyers as 'Clients' where we represent their interests in a transaction, or simply as a 'Customer' where we may be also representing the Seller in a transaction, and are only providing cursory guidance to the Buyer, to facilitate the transaction.

As of December 1st, the 'Customer' relationship will no longer be allowed. You would either be a Client of the Realtor/Brokerage, or opt to be 'Self Represented'. The difference here, is that as a Realtor, I would be forbidden for giving *any* insight, advice, or market-knowledge to any Self Represented parties. They cannot discuss service options, opinions, advice of any kind, or do anything that would encourage a Buyer to rely on our knowledge, judgement or skill. They would completely be acting on their own.

Buyer Representation agreements - "designated representatives" becomes much more critical as of the December 1 implementation, where we clearly describe the duties owed to a Buyer and Seller in every transaction.

Once these changes come into effect, we will be allowed to share some detailed information guides, provided by RECO - the Real Estate Council of Ontario. Linked below is an advanced copy of a standard RECO Information guide, which will replace our current "Working with a Realtor" form we utilize today. It gives a good overview of these basic changes.

Another significant change will be the ability to share the contents of offers on a property, with the Seller's written permission. Sellers can opt-in or out, and can also change their mind - but this option of sharing some non-personal details of offers (i.e. price), can change the dynamic of bidding-wars on desirable properties with multiple interested Buyers. We are sure to see a lot of variation on implementation of this option, and sure to see more on mainstream news channels as the market heats up.

From the Realtors perspective, our services we can offer remain fundamentally the same, however all the years of standardized forms and clauses we rely on, need to be updated to reflect the current terminology and scenarios. Its going to be a bit of the wild-west for a few weeks, while we have a mix of deals that have both old and new forms... There is sure to be significant Agent confusion during the change.

In December, we will share some additional resources on all the changes coming your way - including what's next in January!